Guest post from Heather of My Mothermode

After years of living, um, a little spoiled, I had to face being a stay-at-home mom in the current economy. MoneySavingMom and other financial gurus have been life changers for my family. We are, finally, using a cash system and paying off loans like crazy.

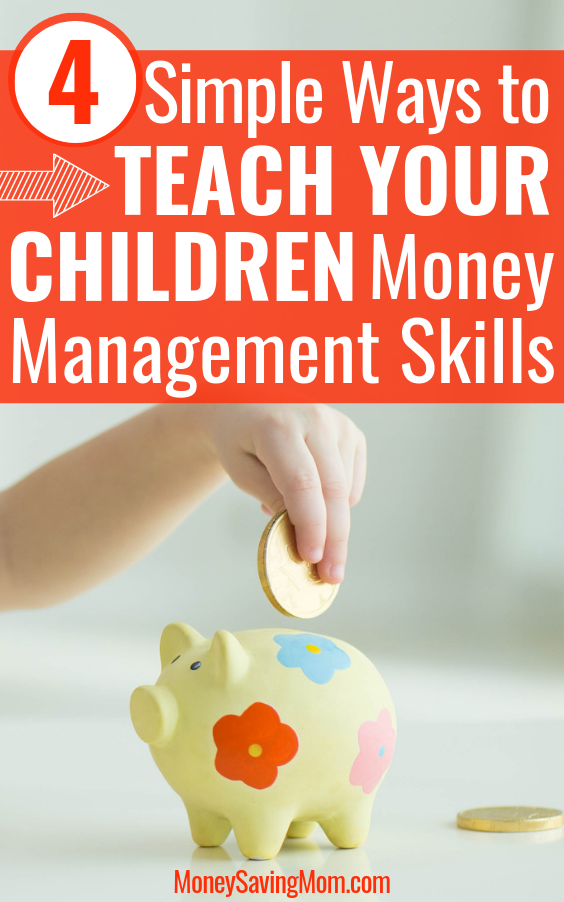

We now have three children, and there is no way I’m letting them coast into the big world with no guidance in money management. From toddlerhood on, here are the steps we have taken to teach them the value of a dollar.

1. Don’t give in to “I wants”.

As soon as they began feasting their bright eyes on colorful trinkets at the checkout, we began to divert their attention. If they do not expect something each time we shop, it makes errands much easier.

We only allow a free sample if the store offers them, and sometimes a quarter machine visit on our way out for good behavior — and the money comes from their own wallets.

2. Teach that money comes from effort.

Our three-year-old recently began insisting, “I want pennies!” My prompt response? To provide him with opportunities to earn pennies!

He was happy to fold towels for his small fistful of pennies. Around age three or four, we introduce a chart with both commissioned and non-commissioned chores. Commissioned chores are for pay; non-commissioned chores are done simply because we should all contribute to the household.

Examples of our commissioned chores are: water the flowers, vacuum, fold towels, and the like. Our non-commissioned chores are: keep your things picked up, help with dinner, care for the animals, and so on.

3. Encourage wise use of money

A small portion of birthday and Christmas money is for their Give, Save, and Spend jars. We explain that many people give 10%, and we let them make the final decision which is usually more like 20-50% for them!

Saving towards a big, but attainable goal is encouraged (such as the guitar my seven-year-old is working toward.) The remainder of the gift funds they receive is put towards sports and other activities.

They have a vested interest in their activities of choice and know that “money doesn’t grow on trees!” We also put their sports uniforms and gear needs on their wishlists to guide family members towards useful presents rather than a load of soon-forgotten toys.

4. Teach the fun in frugality.

We find enjoyable frugal activities to do almost every day. Church activities, library visits, crafting, cooking together, and freebies in our mailbox are just a few ways to have tons of fun on a dime.

Lessons learned? Time management, spirituality, creativity, and resourcefulness, to name a few.

Instruction in money management is confidence-boosting and rewarding. It helps our little ones hone the skills of earning, saving, spending, and giving. These life skills will be priceless, so to speak, as they venture out in the world as young adults.

How do you teach good money-management in your children?

You can find more frugal adventures at My Mothermode, a place where Heather blogs on parenting, saving money, and more.

Great post, I love the jars as a visual reminder of where it goes. I take a different approach to the earning and such, I blogged about it a little while ago (you can read it here https://apeaceoflife.blog/2017/05/26/kids-and-allowance/ if you want 🙂 ) Keep up the good work parents! xx

This is great! These are some fun tips for teaching children about savings and finance. It’s never too early to learn!

Hi Crystal! These tips are spot on! My wife and I often have to remind each other that our 3yr-old should not dictate the terms of our finances to us! 🙂 As soon as he turned 3, we adopted a “commission” framework, so he could begin earning money in exchange for chores/work. This is not an allowance, but a reward for hard work – picking up his room, feeding the dog, etc. We really want him to understand that money is earned, not just handed out. So far it is working well!

I agree most with your second point: ‘Teach that money comes from effort’. My parents raised us well by always letting us know of our situation. They help us understand that we are not that rich to actually buy the unnecessary things that we want. They also made us realize that money is not easily taken, that it takes effort and hardwork to earn them. Now, we grow up with a good financial mindset in mind. We are frugal enough, and know how to do proper budgetting. I am so thankful with how our parents raised us.

Thanks for sharing this post to!

At what age do you think you should start giving a child money and trying to teach them the value of a dollar? My son is 6 and he clearly has no concept of how much a dollar is approximately worth, as evidenced by the time I sent him to school with $20 to buy gifts for family members from his “snowman shop” (or whatever it was called) where they promptly ripped him off by selling him pieces of junk priced at like $3-5 a piece. I’d feel better about it if the money was going to fund the school or something, but it wasn’t, it all went to some for-profit entity that set up that shop in the school. I don’t even know why they allowed it to happen… the whole thing just baffles me in retrospect.

So anyways, yeah, that made me realize that something I take for granted (the value of a dollar) isn’t something that’s just common sense. When should I start trying to teach them that and how do you even really begin to explain it? I can’t even really remember how I learned it or figured it out.

I totally agree with giving allowance. Our 7 year old daughter has chores and receives $7.00 bi-weekly. (Dollar amount equals her age). She has 4 jars distribute as follows: 20% LongTerm Saving (Do Not Touch, after 1 yr, deposit into bank), 5% Charity, 40% Purchase Saving (Save for something specific), 35% Spend. As she gets older, she will be responsible to purchase her clothes and personal items (using the Purchase Savings Jar).

My husband and I recently starting giving our 6 year old son an allowance. We have 3 (mayo) jars labeled saving, spending, and charity. We explained what each was for. We give him $6.00/week based on age. He picked Sunday as his payday and $3.00 is for spending, $2.00 for saving and $1.00 for charity. Once a month we go to the bank to deposit money into saving account and maybe every 3 months we’ll take money to chairty. He decided to help animals so we’ll either donate to a local shelter and/or buy supplies with his money and take it their. We’ll also be volunteering as a family. We’ve also been explaining to him that their are chores you do as part of a family and chores you can do for pay (ie helping Grandpa take down the pool). This system seems to be working well so far in our house and we’ve been doing it for about 6 weeks. All of the money from b-day and christmas has been going to college fund or something that he needs (ie swim class or new clothes).

I just wanted to share how we do it at our house – maybe it’ll give someone some ideas 🙂 We have four children, ages 2-11. In addition to their own bank account, each child has 3 mason jars with the label Save, Spend, Share. Every time they receive any money they divide it into each jar: Save 60%, Spend 30%, and Share 10%. The Save jar is used for longterm purchases such as bikes, educational activities. The Spend jar is used for visits to stores, birthday gifts, etc. The Share jar is counted every 6 months (June and Dec) and the money is donated to the charity of their choice.

We do not pay our children an allowance, but will offer to pay them fairly for odd jobs such as cleaning /sorting Dad’s golf balls 🙂 They also receive money from friends and relatives throughout the year for birthdays and Christmas, and quite frankly, they have quite a bit of money in their jars. They are learning that once the money is gone, it’s gone for good, and they have learned to be very particular about what they choose to spend and save for.

This has been working quite well for us and has created so many opportunities to discuss not only financial issues, but charities, cheap toys, junk food vs healthy food, and alternatives to always purchasing something new.

I wish I had had this article about a month ago! When I took my grandkids shopping with me, they were asking for something at every store. I was very concerned that they had no concept of value, spending, etc. The next day, I devised a “budget” for the allowance I agreed to give them. I had a problem with how to keep up with their money in a child-friendly way. I love your jars and your ideas. Now I can easily keep the money save and visible for them. Thank you!

I love teaching my kids what we do. I made them these cute little wallets with pockets for each: GIVE, SAVE, SPEND. When they get money, we decide together, right then, which money does which job. They are so cute about it. It has been a fun challenge this summer to earn money so they can divide up in the pockets. Here’s a link to my wallets, I sell them in my etsy shop, Miss Money Bags.

https://www.etsy.com/listing/101600384/miss-money-bags-kids-spend-save-give?ref=cat_gallery_7

I love that you are teaching your children how to be frugal. It has only been about 3 years since I started becoming frugal. My children don’t really understand that we are frugal. They love all of our free activities – the river walk, the library, the summer reading program, restaurant promotions, crafts at home, etc. Thanks to coupons, they were stocked with frozen treats during the summer and snacky food now that school has started. I bake and cook from scratch so we always have enjoyable meals. They probably think everyone makes laundry detergent, gardens, and freezer cooks. I think that when they are older and want more expensive items, they will start to understand that they can’t have everything. They do understand that I coupon and my 4 year-old will say, “Mom, when this goes on cheap, can you get it?” I think I will start having them earn some pennies. 🙂

I love the mason jar concept! We have been trying the give/save/spend idea with our kids ever since we finished FPU last fall. I have a few questions about how you do it in your house. Our kids are 8,6,4 so we have the appropriate comission and non-comission chores for them but I find that having “payday” on Saturday isn’t working. I don’t want to teach them ‘instant gratification’ but if they don’t do their chores on tuesday-thay still get paid on saturday for the rest so it sort of backfires. I don’t think they quite learn the lesson since they still get money but the amount changes. When do you have “payday”? Also, now that school is back in session, do you adjust their chores since the schedule is so hectic? Just trying to make this work and would love to hear how you do it! Thanks

Just a thought, but maybe incorporate some kind of chart that displays what chores are paid for and which ones aren’t, as well as the amount paid for each. For every chore that isn’t done, cross off that amount so they can see the actual amount of money they lost out on doing.

Also, I read in a parenting book once about a system that allowed the other siblings the chance to do the chore the first child missed and allowing them to earn the money for that chore instead. That way the chore gets done and the kids have the incentive to get the chore done in a timely manner. I thought it was an interesting idea when I read it, but my kids are only 4 & 2, so a little too young to see how it would work practically.

That’s a great idea about the amount paid being crossed off. We pay five cents per item, which includes homework, piano practice, job of the day- so a 5 in each box would do it. We let Sunday be a day of rest as much as possible, but they still help with the essentials. Maybe a mid-week payday would work, too?

Ours are up by 6:30 am, so there is 1 hour before school to eat, get ready, plus the job of the day (we keep things rolling.) We are also working really hard to have time at home by not allowing their activities to take up every evening.

I have twins that are 5 and a 19month old. In the past year we started the spend, save, give jars for the kids and also made a chore chart. We’ve explained that their are things they do because they are part of a family and things they do that are extra to help. they now love doing chores!! I just used pickle jars I had saved and wrapped construction paper around it. Then took scrapbook stickers for the words and then let the kids use foam stickers to decorate. It was very easy.

We use gift money they get for birthday or christmas towards activities like gymnastics or karate (from the Community Ed which is way less $$) Also we’ll use it towards clothes they need.

I love that when I go out with the kids I rarely here, “I want or Can I have!”. They also have learned about the cost of things. It’s really cute when my 5 year old says, “Mom if you have a coupon can we buy x.” And they are fine with going to the consignment store for “treasures they want.”

Growing up, we always had 3 jars-Jesus, Save, and Spend. We put 10% in Jesus and then split the remainder between Save and Spend. I am SO grateful for parents who taught me to live this way. Thanks to their guidance (and example of living 100% debt free-and yes, that means no mortgage), the only debt my husband and I have is our house which we purchased 8 years ago….and it will be paid off within the next year 🙂 We cannot wait to shout that we are DEBT FREE!!!

Love that your kids have to earn what they get…We’ve often considered allowences, but our own budget is tight, and giving kids an allowence for simply existing is not how real life works. We have often provided opportunities for our boys to earn money for spending, but so many of their friends get allowences that I sometimes wonder if we’re too out of touch. THanks for sharing!

Mary,

Growing up we always got a very small allowance and that was in response to our chores that we always had to do to help with the household – load the dishwasher, clear the table, help clean the house each week, etc. The chores changed as we got older of course, but the allowance never did. That way, we still got an allowance, but we had to earn it too. If we didn’t do the “help with the household” chores, then we didn’t get our allowance. Just a thought but I think it was a pretty good system.

I point out the prices of things and make comparisons so my 5yo can understand. When the ice cream truck drives by, she gets excited hoping to get one. I pointed out that the truck charges $2 for one treat. But I can buy a container of ice cream or a box of popsicles that is enough for our whole family to share for a couple of days for that same $2 when I go to the store and buy it on sale and with a coupon. So $2 for 1 treat now, or be patient and wait for a sale and get 10 treats worth later. She loves Icee drinks and always wants one whenever we’re in a store that sells them. Once in a while I will purchase one, other times I tell her that if she wants one, she has to use her own spend money to have it.

Those jars are super cute! Such a creative way to help kids keep track of their money, especially since they can see just how much they’ve been saving through the glass. Also, the commission vs. non-commission chores idea is super neat. I’ve never heard of that before, though it does make total sense. My son is still super young, but this is definitely something to keep in mind for the future. Thank you!

I’m wondering if anyone else struggles with relatives who are very generous with cash gifts to their children? My husband and I are from divorced families, and while my mom and stepmom stick to practical gifts, my out of state in laws send very generous checks for birthdays and Christmas.

In the past, we’ve used this money for things like zoo passes and sports lessons, but as our boys are getting older they’re increasingly aware of this loot that comes in the mail and feel like it should be their choice as to how to spend it. Our 9 year old would like a Nintendo DS3, and while part of me thinks he should be able to get what he wants with money intended for him, part of me is also very bothered by how Easy it is-between my husband’s dad and stepmom, his grandma, and his mom and stepdad, our son would easily have more than enough on Christmas morning without having to do a lick of work or saving the rest of the year.

I hope I don’t sound like I’m terribly unappreciative, here. I fully understand their desire to give something to our boys, especially since they don’t seem them often, and I truly do appreciate it.

I also hope it doesn’t sound like my kids are horrible monsters! They are pretty spoiled, but we do make them do chores, and they do give money to others. They are, however, keenly aware of the latest gadgets and toys and how much they cost.

I would love to hear any input if it isn’t too off the topic. I really thought we had solutions when they were younger, but it’s gotten much trickier.

If I had a situation like this I would likely simply state that so-and-so’s gift is going to be used for such and such lessons or zoo pass or whatever is best for their enrichment. Maybe a small portion can be set aside for them to put towards whatever gadget they are wanting. You could also have a little talk with the out of state relatives about how much you appreciate the monetary gifts but that maybe it’s time that a note arrives with the gift “suggesting” how it should be spent, and that maybe that note could specify “college fund”, “lessons”, etc. That could backfire though if the giver thinks that it’s fine for the kids to just take the money to the store for the latest electronics and toys.

That is tricky! I sure see your value to teach your kids about hard work to earn what you want. I think since it is a gift intended toward them, it is hard to dictate what it needs to be spent on. I also would tread with caution in asking them to tell the children what to spend it on. I think that is a strange lesson for them to think it is ok to tell people what to do with a gift. I am guessing these relatives want him to be able to spoil himself with the latest and greatest. Maybe just applying the same philosophy of saving/giving/buying to the gift amount, even if this still results in the immediate satisfaction of buying what he wants. Or even doing volunteer work as a family to recognize those in need to help them understand how lucky they are! As adults we all have different salaries etc and some people do have more and can get “things” easier than others, those people still have to learn to manage money. I think kids learn a lot by just watching parents be responsible with money. At some point he is bound to blow it all right away and then later in the year need/ want more. That is a great time to reference that money. This is the time for kids to make and learn from financial mistakes.

My children get fairly large cash gifts from their grandparents, too. Their one grandmother actually deposits $50 into an account for them for their birthdays. And she puts a receipt in with the birthday card. The kids know it’s there, but it’s not right in front of them, so they aren’t tempted to spend it. My 10-year old has a lot in her account right now!

The other grandparents give them cash or a check in their card. When we receive it, we decide how much of it they can spend frivolously and how much goes into their savings account. For example, we’re Jewish, so for Hanukkah, the kids get $80 ($10 for each night). Of that, we suggest that they put away $50 into their savings account and can keep $30, which is still a big sum, especially since they also get gifts from aunts and uncles, an allowance, birthday gifts, etc. They can still work towards saving up for a specific item.

Have a family discussion about how gift money should be spent. Tell your kids the areas that you would like to see their money go towards such as spending money, savings or college savings, giving, etc. Talk about the importance of saving money for the future even if it seems so far away and also the importance of giving to your church or those less fortunate. See if everyone can come to a decision on how it should be used, such as 50% to spend anyway they’d like (which can be blown right away or saved for a larger purchase in the coming months), 30% for savings, 20% for giving. If you can come to an agreement BEFORE the money rolls in, then you can gently remind them of the decision made as a family in where to put the money. If you wait til the money is in their hands, it will be hard to have an open discussion in the heat of the moment when greed & DS3 dreams are bouncing in their heads.

Obviously, I think it is perfectly acceptable to guide your children in how to use their gift money! The fact that they are lavished with more than is healthy for their age makes it imperative that you teach the value of money, so they do not become spoiled or begin to feel entitlement. Some of my family members give my children money for Christmas or birthdays to put into a college savings account for them, or send us a check and tell us to put some into college savings and let them spend some, too. Even if your relatives do not specify how to use the money, it is teaching your children responsibility with money and self control to save and give some of what they receive. As adults we don’t often see the need for an emergency savings account when we have good steady jobs and everyone is healthy, but we are wise stewards when we anticipate the uncertainty of the future & save accordingly. Your kids don’t fully understand the cost of college books or a high school trip or a car, but learning to save for things that seem so far away is a lesson they’ll use for life!

Thank you, gals so much for all your wisdom.

I’m realizing we need to involve the kids in the conversation about this money this year, and we need to have a plan before the big day.

I appreciate you all taking the time,and you have definitely given me a lot to think about!

We have the gift money, as well. It is primarily used for activities. For my daughter, every bit is needed for dance. For my toddler, all of it goes towards preschool savings! My oldest son only needs a portion of it for his activities, so the remainder has been used for summer day camp, and we may have him begin to save for a car or college. We do have to work hard to keep the lesson going when others give them money for school fairs or vacation souvenirs.

And, as I mentioned before, we do allow a portion to go into the jars for our older children. But not much, since they really need it for those activities!

Thanks so much! We were just thinking that it’s time to make a “Giving/Saving/Spending” bank, but can’t afford the ready-made one we know about right now

When the kids were smaller, one of the banks gave away this piggy bank that had 4 slots — give, save, spend and INVEST! We would break down any money the kids got, and put at least 10% in the give, at least 10% in the save, at least 10% in the invest, and the rest could be put in the spend portion. Since I admit to have NO know-how in investing, we put the invest money in a savings account for the kids where it earns a little bit more than just ‘saving’ in the piggy bank. It is our hope to eventually learn how to teach the kids to actually invest, too.

Thanks for the post and the advise!!!

I love that you let the children choose what percentage to give/save/spend. I think that helps them become more responsible with their money than forcing them to split it a certain way. I like to think that I will guide my children toward maturity or responsiblity but that I cannot force it upon them or they will often rebel.

Also, make sure you have your child check out Craigslist for a used guitar. I see children’s ones on there all the time for 1/3 to 1/2 of new, and many of them are hardly even used! I just bought one for myself on CL, and it was less than 1/2 of a new one.

Nice post!

It is certainly a process for them to make these decisions. Since penning this in July, her savings goal has actually gone from guitar to trampoline to treehouse (which requires a key element- the carpenter!) And she enlisted her brothers contributions for the latter two. A goal that is attainable within a few months is ideal.

Thanks!